The Digital Bank Explosion via Banking-as-a-service

Wave upon wave of FinTech...

There's a lot of activity around the globe. Newer players are popping up in LatAm, Africa, Middle East. Globally, digital banks have raised over $2 billion in VC funds in this year alone. Massive stuff.

Banking-as-a-service (BaaS) As Fuel

In recent news, Stripe and Revolut have come up with even greater competitive offerings. Specifically, Revolut will go head-to-head with Stripe's core services such as checkout software and taking payments online.

Stripe has fired their own salvo, offering loans as a service. New digital banks can tap on their infrastructure to offer loans. Additionally, Stripe can do their own via Stripe Capital, basically offering loans for retail and businesses. Win-Win.

Stripe itself teams up with Citibank and Goldman Sachs to offer banking services. Called Stripe Treasury, it’s basically MatchMove's business model, all via APIs. In this case, even a new entrant sees their model being challenged by incumbents.

This allows Stripe's 'Banking' customers to send, receive, and store funds for customers. The partnership is a strong one, with plans to expand in the US and globally. Win-Win-Win.

We also saw Apple partnering with Goldman for their banking accounts via their Marcus product.

It is a smart way to hedge against disruption in banking. If you cannot beat or out-innovate them, join them in some way!

BaaS acts as a platform where new digital banks leverage on for the rest of their operations. This lowers their initial start-up cost and lets them focus on the marketing and operations side of things.

If you were a start-up, the cash burn and regulatory burden can quickly eat up your funding rounds.

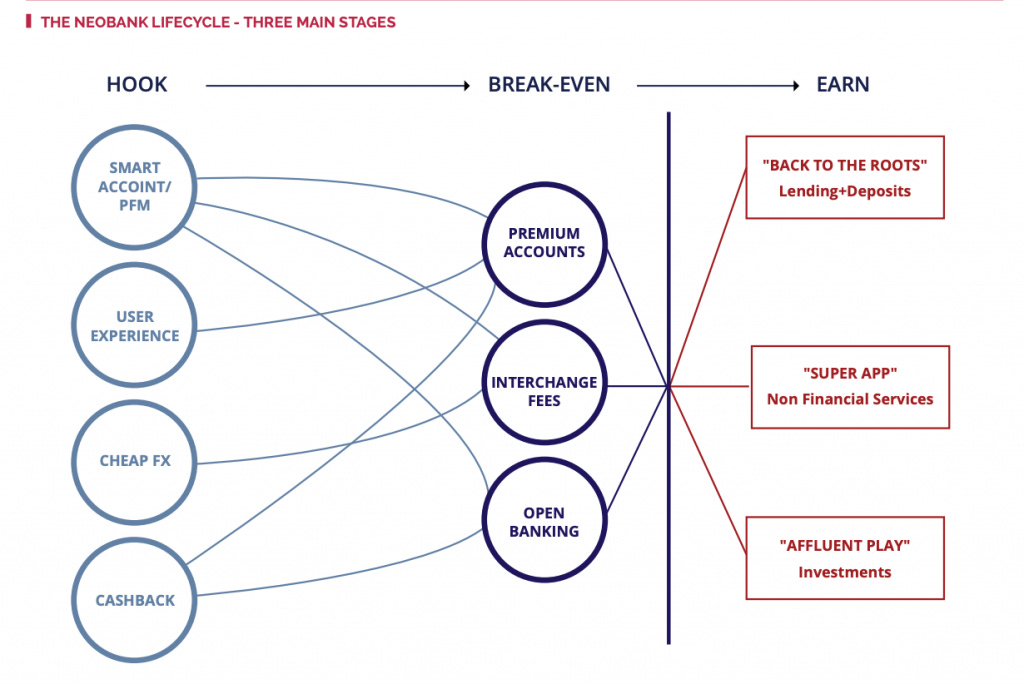

And having the word 'bank' does not immediately makes your firm profitable. A digital bank is still a fledgling start-up, with the same risks, if not higher than technology ones. The key is to break-even as fast as possible, or be very well-funded, else risk being competed away.

So How Would The Legacy Banks Make Money?

I believe it will be a game of volume and market share. The more deposits, transactions or any service that a bank can take now, and manage at scale, the greater chances their chance of inducing customer lock-in later.

This has an advantage against other potential competitors who may wish to enter or take away their customers.

What matters are other components of the banks' products, such as their unique proposition, customer satisfaction, and so on.

It is a messy fight - recall the fights of how Grab, SEA, and other start-ups practically "throw money at the problem" to get market share? That's how it would be, especially in the early stages (say 1-3 years), until there are clearer winners. The customers vote with their wallets after all!

You have start-ups taking aim at established businesses, you have incumbents fighting against start-ups... the innovation cycle is likely to increase and price/rates wars to ensue.

Where Does Banking Go From Here?

The likelihood is that banks become less centralized. You would still have the "Mega" banks, stemming from the FAANGs, or "Old Guard" the likes of Citibank and Goldman.

You also have a disparate spread of companies offering many banking services, something like a microservice architecture - and even cross collaborations amongst these two types of entities.

Apart from the structure of the market, AI as part of bank operations will be increasingly common. Innovative offerings or those required to compete with incumbents require AI capability.

There would be diminishing returns to this approach, and yet it is the basic requirement to even begin to compete - as such, research and development costs are likely to increase, but probably not as fast as the cost savings from regular banking operations.

Regulation and Nationwide Standards

Of course, Fintech won't run unchecked. Open as many new products as you want, you would still need to follow the rule of law. Whether this is something Fintech companies can accommodate will be to their advantage.

Different Responses By Geography

Recently, China is seen to increase its regulatory scrutiny, especially on FinTech platforms.

However, we see the opposite of "Western" countries such as the US or Europe. US tends to be more open to innovation, while Europe seems to be busy dealing with EU and Brexit, Covid, and domestic issues specific to each country.

There is progress in Europe however. Nordigen has opened access to European banking APIs, allowing users to access major European bank data with one API, thereafter categorizing data into income and expenses.

Why is this a big thing? The EU bloc has a stringent set of criteria. In particular the PSD2 directive: A regulation to make payments more secure. Nordigen supports 300 European banks, and covering 60-90% of the population in the countries it operates in, so this is no lean feat.

E-Commerce As A Key Driver

Digital Yuan was implemented through JD.com in the 12.12 sales in 2020. A fintech affiliate called JD Digits launched a pilot program. Customers can pay for certain items with the digital yuan, whereby 100,000 digital cash vouchers worth 20 million yuan total would be issued to residents of Suzhou city.

In doing so, this can also test the concept of Universal Basic Income - except this reduces the cost of living for some, rather than giving outright cash. The net effect is that people still have more cash in their wallets than before, and can serve similar purposes.

Think of payments as another form of electronic transactions just as e-commerce is. You basically have an escrow, a sender, and a receiver. Behind the scenes is a complicated approval process, but this is handled smoothly by blockchain.

The result? Increased transparency in transactions, and ease of tracking by the Government. This means if companies can successfully use a blockchain infrastructure for their payments handling, it is likely they will be allowed to produce more lucrative products.

Due to the digital transactions of E-Commerce, tracking, issuance, and reversal of transactions are much easier. How this permeates into physical transactions would be a matter of time, and use case adoption.

The digital yuan has been used in more than four million transactions, worth a total of about 2 billion yuan ($306 million), as of early last month, according to People’s Bank of China Governor Yi Gang.

The central bank kicked off tests for the online renminbi in some cities in April to bolster its status as a global currency and to help control the domestic economy as it rapidly goes digital.

Singapore Specifically

JP Morgan has realized the trend for e-commerce, setting up their Onyx unit that works directly on Project Ubin. The project currently leans towards corporate settlements. Once tested well, they may go into retail transactions i.e. e-commerce, offering these to the wider market.

What this means is that any company with an e-wallet now can tap on PayNow infrastructure. Companies themselves can take payments via their corporate bank account with PayNow. Integrated with blockchain with a variant of Project Ubin, transactions and processing can be made seamless!

Similar to Nordigen, Singapore moves a step in the same direction with SGFinDex, allowing bank account information to be shared across banks.

This is powerful because KYC can be done much easier with the combined information, forming a flywheel effect for FinTech companies that are ready to integrate with the Government's services.

Note that this was built by the MAS and Smart Nation and Digital Government Group (SNDGG) of Singapore, and not a start-up!

Who wins?

The Consumer. Retail banking will become extremely competitive, to the point smaller players without scaling advantages will eventually drop out, leaving new contenders worth of the mantle. The "Megas" may see their market share being chipped away, but are likely to stay in the game.

Banking for consumers becomes embedded in the entire lifecycle of how they consume on the Internet - how they shop, travel, send items, pay bills, trade, run their business - each touchpoint may see banks involved in one way or another, and more often due to the "Microservice" nature.

Companies, whether SME or MNCs, may also be spoilt for choice. Having historically low-interest rates and a heightened amount of lending players, it would be easier to negotiate for lower rates or more attractive packages.